The good news is that Joe Biden has not embraced many of Bernie Sanders’ worst tax ideas, such as imposing a wealth tax or hiking the top income tax rate to 52 percent..

The bad news is that he nonetheless is supporting a wide range of punitive tax increases.

- Increasing the top income tax rate to 39.6 percent.

- Imposing a 12.4 percent payroll tax on wages above $400,000.

- Increasing the double taxation of dividends and capital gains from 23.8 percent to 43.4 percent.

- Hiking the corporate tax rate to 28 percent.

- Increasing taxes on American companies competing in foreign markets.

The worst news is that Nancy Pelosi, et al, may wind up enacting all these tax increases and then also add some of Crazy Bernie‘s proposals.

This won’t be good for the U.S. economy and national competitiveness.

Simply stated, some people will choose to reduce their levels of work, saving, and investment when the tax penalties on productive behavior increase. These changes give economists the information needed to calculate the “elasticity of taxable income”.

Simply stated, some people will choose to reduce their levels of work, saving, and investment when the tax penalties on productive behavior increase. These changes give economists the information needed to calculate the “elasticity of taxable income”.

And this, in the jargon of economists, is a measure of “deadweight loss.”

But now there’s a new study published by the Federal Reserve which suggests that these losses are greater than traditionally believed.

Authored by Brendan Epstein, Ryan Nunn, Musa Orak and Elena Patel, the study looks at how best to measure the economic damage associated with higher tax rates. Here’s some of the background analysis.

The personal income tax is one of the most important instruments for raising government revenue. As a consequence, this tax is the focus of a large body of public finance research that seeks a theoretical and empirical understanding of the associated deadweight loss (DWL). …Feldstein (1999) demonstrated that, under very general conditions, the elasticity of taxable income (ETI) is a sufficient statistic for evaluating DWL.

…It is well understood that, apart from rarely employed lump-sum taxes and…Pigouvian taxes, revenue-raising tax systems impose efficiency costs by distorting economic outcomes relative to those that would be obtained in the absence of taxation… ETI can potentially serve as a perfect proxy for DWL…this result is consistent with the ETI reflecting all taxpayer responses to changes in marginal tax rates, including behavioral changes (e.g., reductions in hours worked) and tax avoidance (e.g., shifting consumption toward tax-preferred goods). …a large empirical literature has provided estimates of the individual ETI, identified based on variation in tax rates and bunching at kinks in the marginal tax schedule.

And here are the new contributions from the authors.

… researchers have fairly recently come to recognize an important limitation of the finding that the ETI is a sufficient statistic for deadweight loss… we embed labor search frictions into the canonical macroeconomic model…and we show that within this framework, a host of additional information beyond the ETI is needed to infer DWL …once these empirically observable factors are controlled for, DWL can be calculated easily and in a straightforward fashion as the sum of the ETI and additional terms involving these factors. … We find that…once search frictions are introduced, …DWL can be between 7 and 38 percent higher than the ETI under a reasonable calibration.

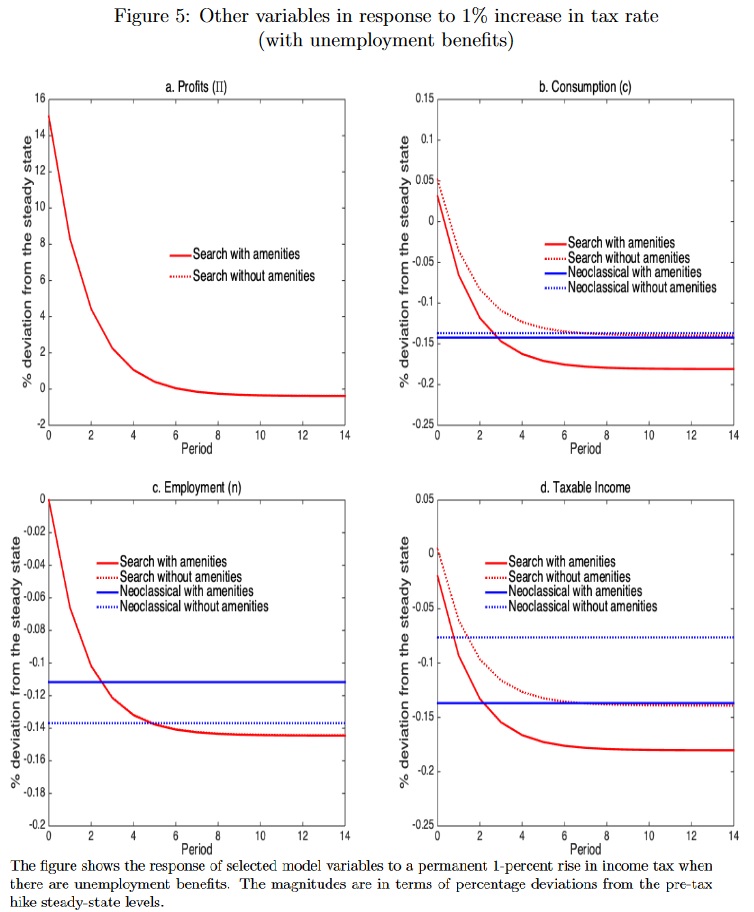

To give you an idea of what this means, here are some of their estimates of the economic damage associated with a 1 percent increase in tax rates.

As you peruse these estimates, keep in mind that Biden wants to increase the top income tax rate by 2.6 percentage points and the payroll tax by 12.4 percentage points (and don’t forget he wants to nearly double tax rates on dividends, capital gains, and other forms of saving and investment).

Those are all bad choices with traditional estimates of deadweight loss, and they are even worse choices with the new estimates from the Fed’s study.

So what’s the bottom line?

The political impact will be that “the rich” pay more. The economic impact will be less capital formation and entrepreneurship, and those are the changes that hurt the vast majority of us who aren’t rich.

———

Image credit: Max Pixel | CC0 Public Domain.