The Congressional Budget Office just released its new long-run fiscal forecast.

Most observers immediately looked at the estimates for deficits and debt. Those numbers are important, especially since America has an aging population, but they should be viewed as secondary.

What really matters are the trends for both taxes and spending.

Here are the three things that you need to know.

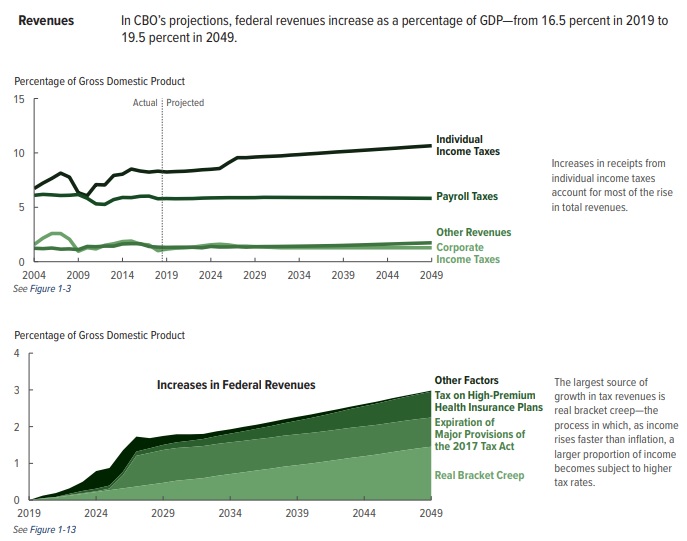

First, America’s tax burden is increasing. Immediately below are two charts. The first one shows that revenues will consume an addition three percentage points of GDP over the next three decades. As I’ve repeatedly pointed out, our long-run problem is not caused by inadequate revenue.

The second of the two charts shows that most of the increase is due to “real bracket creep,” which is what happens when people earn more income and wind up having to pay higher tax rates.

So even if Congress extends the “Cadillac tax” on health premiums and extends all the temporary provisions of the 2017 Tax Act, the aggregate tax burden will increase.

Second, the spending burden is growing even faster than the tax burden.

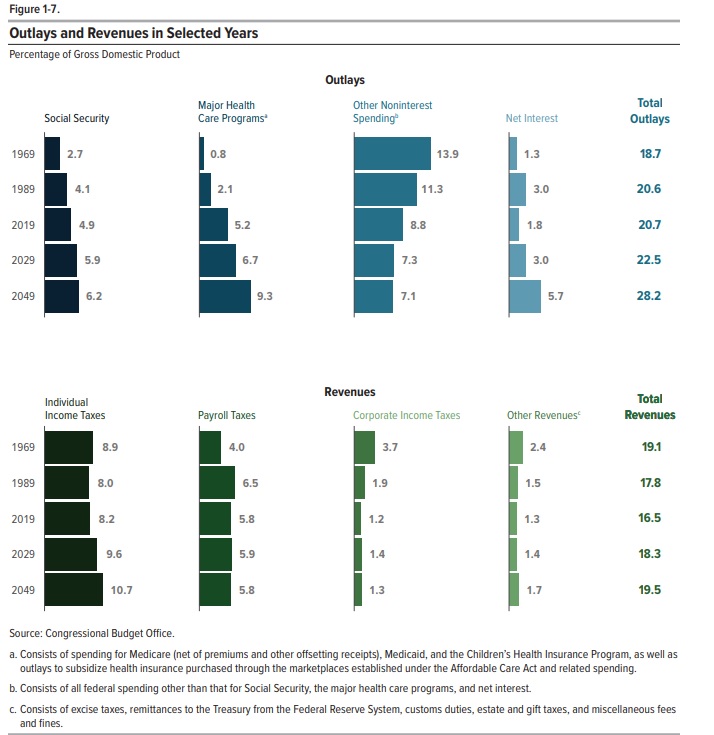

And if you look closely at the top section of Figure 1-7, you’ll see that the big problems are the entitlements for health care (i.e., Medicare, Medicaid, and Obamacare).

By the way, the lower section of Figure 1-7 shows that corporate tax revenues are projected to average about 1.3 percent of GDP, which is not that much lower than what CBO projected (about 1.7 percent of GDP) before the rate was reduced by 40 percent.

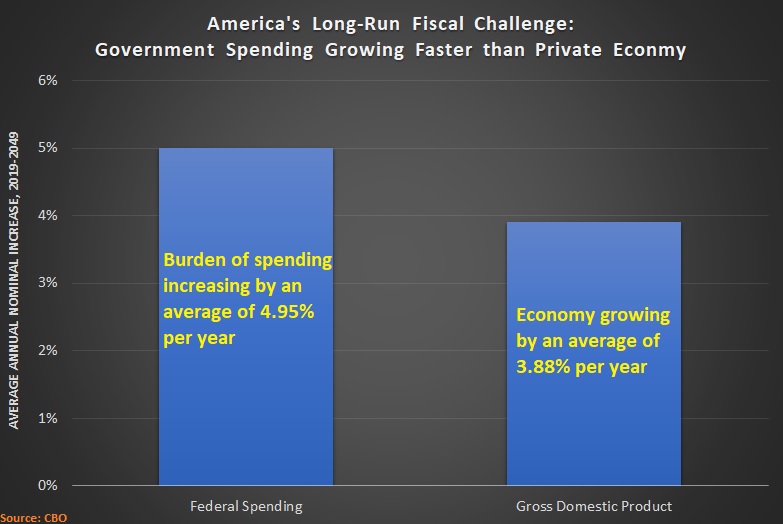

Third, we have our most important chart.

It shows that the United States is on a very bad trajectory because the burden of government spending is growing faster than the private economy.

In other words, Washington is violating my Golden Rule.

And this leads to all sorts of negative consequences.

- Government consumes a greater share of the economy over time.

- Politicians will want to respond by raising taxes.

- Politicians will allow red ink to increase.

The key thing to understand is that more taxes and more debt are the natural and inevitable symptoms of the underlying disease of too much spending.

We know the solution, and we have real world evidence that it works (especially when part of a nation’s constitution), but don’t hold your breath waiting for Washington to do the right thing.