It was widely assumed that, were SCOTUS to rightfully strike down Trump’s IEEPA tariffs (including those from his “Liberation Day”) as illegal executive overreach, the President would respond by reconstituting much of his protectionist tariff regime using other statutory authority.

Trump is trying to do just that following the SCOTUS ruling in Learning Resources, Inc. v. Trump by announcing a new 10% global tariff, and then threatening to raise it to 15%.

This doesn’t invalidate the importance of the Supreme Court’s ruling, not just because it’s a powerful affirmation of major questions doctrine (used previously to strike Biden’s student loan forgiveness) and its role in hopefully forcing Congress to take seriously its Constitutional obligations once again, but also on the narrower policy questions of what tariffs will apply and at what rates.

While there are other statutory bases for imposing tariffs, like Section 301 of the 1974 Trade Act and Section 232 of the 1962 Trade Expansion Act, they are more procedurally burdensome, hence why the administration avoided using them in the first place.

But Trump isn’t relying on those authorities for his latest across the board tariffs.

Instead, the administration is citing Section 122 of the Trade Act, which provides for temporary tariffs (up to 150 days without Congressional action) in the case of “large and serious United States balance-of-payments deficits.”

The relevant legal question, and thus likely the contention of the next round of lawsuits, is what that language means and whether, as the administration now claims, it includes trade deficits.

By nearly all accounts, it does not. From NTU’s Bryan Riley:

Section 122 does not define the phrase “fundamental international payments problems.” However, its meaning is clear from historical context. The provision was designed to address international payments crises that may arise under systems of fixed or managed exchange rates.

…Section 122 only makes sense under a fixed exchange rate regime, under which the United States could experience a shortage of reserves needed to cover its international obligations.

…In March 1973, the United States adopted a system of floating exchange rates, which allows currency values to adjust according to market forces. This eliminated the need for the government to maintain reserves to defend a fixed dollar value. As economist Milton Friedman explained, “a system of floating exchange rates completely eliminates the balance-of-payments problem. The [currency] price may fluctuate but there cannot be a deficit or a surplus threatening an exchange crisis.”

As a result, Section 122 was effectively rendered obsolete and has never been invoked.

These new tariffs are even more clearly illegal than Trump’s IEEPA tariffs.

…In Section 122, Congress endowed the president with narrow, temporary authority to impose tariffs “to deal with large and serious United States balance-of-payments deficits” (emphasis added). What Trump is complaining about — something he insists is a crisis but is not — is the balance of trade, not of payments. The United States does not have an overall balance of payments deficit, much less a large and serious one.

A trade deficit between the U.S. and a foreign nation occurs, mainly in connection with goods (which is just one aspect of international commerce), when imports are greater than exports. This is not really a problem for a variety of reasons — e.g., a trade deficit results in an investment surplus, the U.S. is a major services economy and often runs exported services surpluses that mitigate the imports deficit in goods, etc.

The balance of payments is a broader concept than the balance of trade. It accounts for all the economic transactions that take place between the United States and the rest of the world. Even without getting into every kind of transaction that entails, suffice it to say that foreign investment in the United States, coupled with the advantages our nation accrues because the dollar is the world’s reserve currency, more than make up for the longstanding trade deficit in goods.

Our overall payments are in balance. There is no crisis.

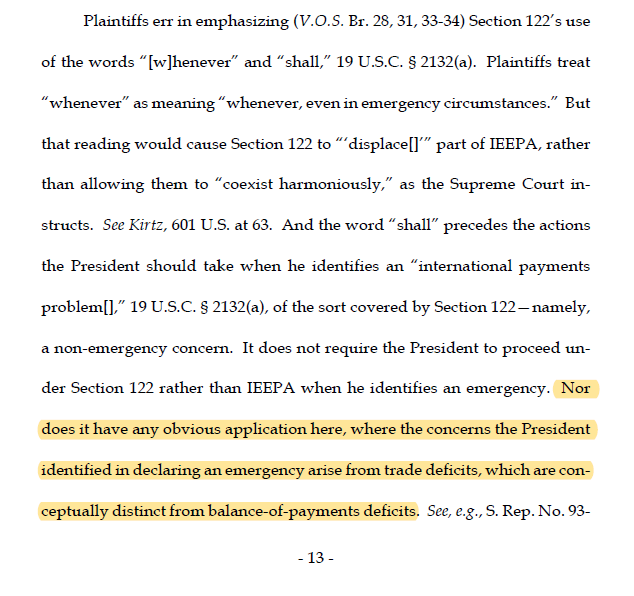

But it’s not just economists pointing this out. The Trump DOJ’s own legal filings admitted as much:

Oops.

Legal debates aside, the question remains: what does the administration hope to achieve? Trump’s original tariffs, before they were rightfully invalidated, failed to accomplish any of the often conflicting goals cited by proponents. The “trade deficit” is unchanged. Manufacturing employment is down. And Americans are paying.

So why does Trump do this? Unfortunately, as Scott Lincicome explains, he just likes tariffs. He has a long-held understanding of global trade that is fundamentally flawed. He thinks trade is zero-sum and that if Americans buy more than they sell abroad, then it means that they are getting “ripped off.” But he is simply wrong about trade deficits.

He also just likes being able to unilaterally create chaos that forces world leaders to give him attention, along with the power to punish those who he finds insufficiently obsequious. That’s why he chooses the tariff authority that seemingly affords him the most arbitrary power, rather than ones that he could actually legally defend.