This first chart is from the International Monetary Fund and it shows that corporate tax revenues increased as a share of GDP as tax rates were reduced.

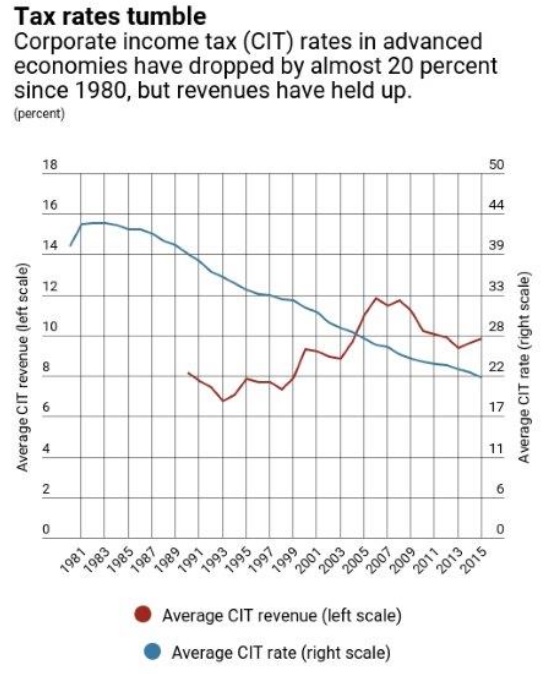

This second chart from the Organization for Economic Cooperation and Development shows something similar, with tax revenues staying the same as a share of economic output as tax rates declined.

So I went to the OECD’s latest edition of Revenue Statistics and did a screenshot of this data showing that tax revenues are now a much larger share of GDP today, even though (or perhaps because) corporate tax rates are much lower.

So why am I sharing all this data?

Because Jane Gravelle at the Congressional Research Service just authored a report claiming that huge increases in corporate tax rates would generate more revenue.

I’m not joking. Here are some excerpts.

Economists have long recognized that there are behavioral responses to the corporate tax, and that these responses have implications for the efficiency of the economy and the burden of the tax, as well as how much revenue a tax increase might raise. This report examines the research surrounding the revenue-maximizing corporate tax rate and explores implications for federal tax policy. …While the empirical studies directly estimating the revenue-maximizing tax rate have not yet developed the ability to reliably estimate a revenue-maximizing corporate tax rate, simple theoretical insights indicate that a revenue-maximizing corporate tax rate is much higher than either the current 21% rate or the 35% rate before the 2017 rate cut. Such a rate is probably no less than 70%, a finding consistent with most of the results of the alternative approach of estimating the elasticity of the tax base with respect to the tax rate.

Jim Carter was not impressed by the CRS publication.

Here are some excerpts from his column in the Daily Caller.

Washington’s tax bureaucrats want you to believe you can tax your way to prosperity. History says otherwise. The Congressional Research Service’s April 21 report, Corporate Taxation: The Revenue-Maximizing Tax Rate, uses a model to estimate the corporate tax rate at which corporate tax revenue is maximized. Under its baseline assumptions, that peak occurs at roughly 70% or higher.…In a globalized economy, the average OECD corporate tax rate has fallen from 47% in 1980 to 23% today… A landmark 2008 OECD study concluded that corporate taxes are the single most harmful form of taxation for long-run economic growth. A government chasing peak revenue extraction from the most growth-destructive tax in the modern economy is optimizing for the wrong variable. The CRS report also leans heavily on static revenue estimates and gives little weight to dynamic effects. It says raising the corporate rate from 21% to 28% would produce a “static revenue increase” of 33%, then argues that behavioral responses are too small to matter. …Those who advocate dramatically higher corporate tax rates will cite the CRS report as intellectual cover for a policy that real-world evidence does not support. …America does not have a revenue problem. It has a growth problem. And no government in history has taxed its way into prosperity.

P.S. On a separate note, Jim makes a critical point about the difference between the revenue-maximizing rate of taxation and the growth-maximizing rate of taxation.

The CRS report’s central mistake is simple and damning: revenue-maximizing and economically optimal are not the same thing. Economists have long recognized that the revenue-maximizing point on a Laffer curve sits well above the growth-maximizing point. A rate can keep squeezing additional revenue past the point where it begins seriously discouraging investment, productivity, and wages.

P.P.P.S. If you want data-driven evidence for the Laffer Curve, click here for evidence from developed nations and click here for astounding evidence from Ireland.