The main symptom of that policy is what is known as third-party payer, which occurs when a consumer buys with other people’s money. And that is a perfect description of how government has screwed up our health system.

For all intents and purposes (see cartoon), we don’t allow markets to function in health care.

Instead of buyers and sellers directly interacting, government policies have imposed layers of intervention.

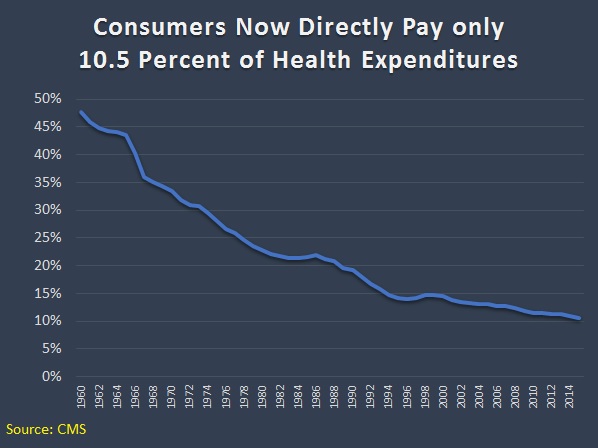

Since I realize some people may not view my cartoon as evidence, here’s a chart showing the dramatic increase in third-party payer in America.

And this chart is from 2017. I’m guessing the data is even worse today (though I hope my assumption is wrong).

I’m not the only person who recognizes this problem. Far from it.

Dominic Pino wrote about the healthcare exclusion’s pernicious effect in 2023. Here are some key passages from that National Review column.

Excluding employer-provided health coverage from the income-tax base contributes to all sorts of problems with U.S. health care. …it’s really a classic story of unintended consequences. …Rather than getting money from their employers to spend on anything, including health insurance, most working Americans have part of their pay withheld from them and used by their employers to purchase group health insurance. …Other forms of insurance are not treated this way. People don’t risk losing their home insurance if they lose their jobs. Employers don’t select car-insurance plans for employees to use. Only employer-provided health insurance is exempt from the income tax, so workers’ health insurance is entangled with employment in a unique way. …Transferring control from workers to employers, as the tax code effectively does, distorts the health-care market in all sorts of ways. It lowers price sensitivity among consumers, which contributes to high prices.

As Dominic points out, and as the video explained, the healthcare exclusion results in lower wages for workers.

And here are some excerpts from an article last September by James Capretta and Bryan Dowd of the American Enterprise Institute.

The full exclusion of premiums paid for employer-sponsored insurance (ESI) from income and payroll taxation is profligate. The Office of Management and Budget (OMB) estimates it cost the Treasury $0.3 trillion in 2023 and will drain another $5.6 trillion from the government’s receipts over the coming decade. It is far and away the most expensive tax break in federal law. …encouraging excessively generous and loosely-managed health insurance at the expense of taxable wages and salaries. …The Affordable Care Act (ACA), approved by Congress in 2010, imposed…“Cadillac tax,” a new levy on employers…a somewhat clumsy effort to limit the tax subsidy without admitting that was the objective. It still faced stiff resistance from businesses and labor unions, which led to Congress repealing it in 2019.

Since Capretta mentioned Obamacare’s Cadillac Tax, I can’t resist mentioning that I liked that provision.

And the Cadillac Tax would have had a big effect, as shown by this visual.

The goal of the tax was not to raise revenue, but instead to discourage over-insurance.

In a logical and sensible system, health insurance would be like auto insurance or home insurance. In other words, it should be a way for consumers to protect themselves against large and unexpected costs.

Today, thanks to government, we have health insurance that is akin to a pre-paid, all-you-can-eat buffet.

{kind=link}