If you asked a reasonably competent economics student to explain why there was a surge of inflation in the eurozone in 2022, that person presumably would be familiar with Milton Friedman’s wisdom and immediately would investigate whether there was a mistake in monetary policy.

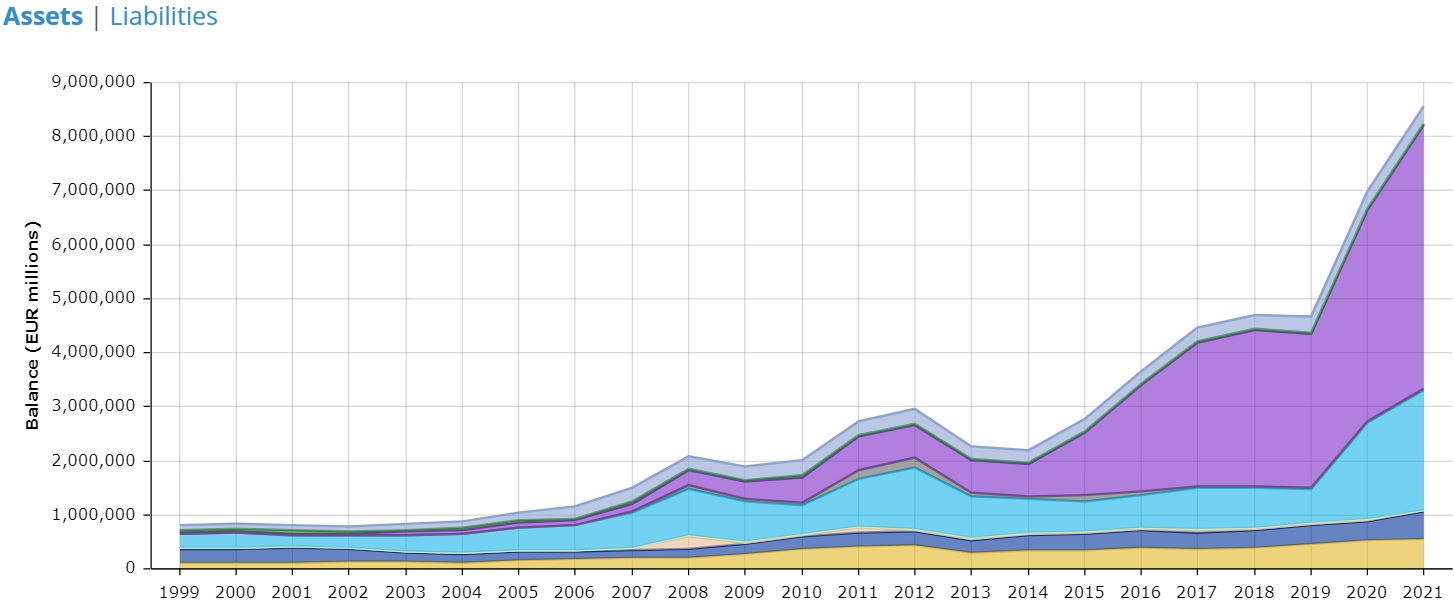

Lo and behold, our student would look at the European Central Bank data and say, “what the [expletive deleted], the ECB almost doubled its balance sheet in 2020 and 2021, so of course all that money creation led to rising prices.”

But what if, instead of asking a competent student, you asked some economists at the European Central Bank to answer the same question? Would they reach the obvious conclusion?

Based on a new study from the ECB, it appears the answer is no.

…euro area inflation since 2021 has been driven by both supply and demand factors, with the former playing a primary role. Supply-side shocks were mostly related to energy and food price shocks, partly due to the invasion of Ukraine. At the same time the euro area was hit by an inflationary shock stemming from the combination of pent-up demand for goods and services that accumulated due to subdued spending and excess saving during pandemic lockdowns, and shortages of these goods due to supply chain disruptions. According to the model these shocks exhibit a large degree of persistence; other supply-side shocks, like energy and food, generally have a more temporary impact on price inflation, as those cost-push shocks also reduce income and, hence, aggregate demand.

This is professional malpractice. Though, given the crass blame-shifting by the the political hack who now is in charge of the ECB, I guess we shouldn’t be surprised by such sloppy analysis. For the economics profession, this is sort of like having arsonists investigate fires.

And in case you think I’m selectively excerpting a passage to make the ECB look bad, I invite you to search the study for “balance sheet.” Those two words are completely absent.

Moreover, I did a search for “monetary policy” and got some hits, but none of them were about the ECB’s near-doubling of its balance sheet.