I narrated a six-minute video in 2009 to explain why America’s fiscal problem is spending rather than red ink. Here’s the same message in just 51 seconds.

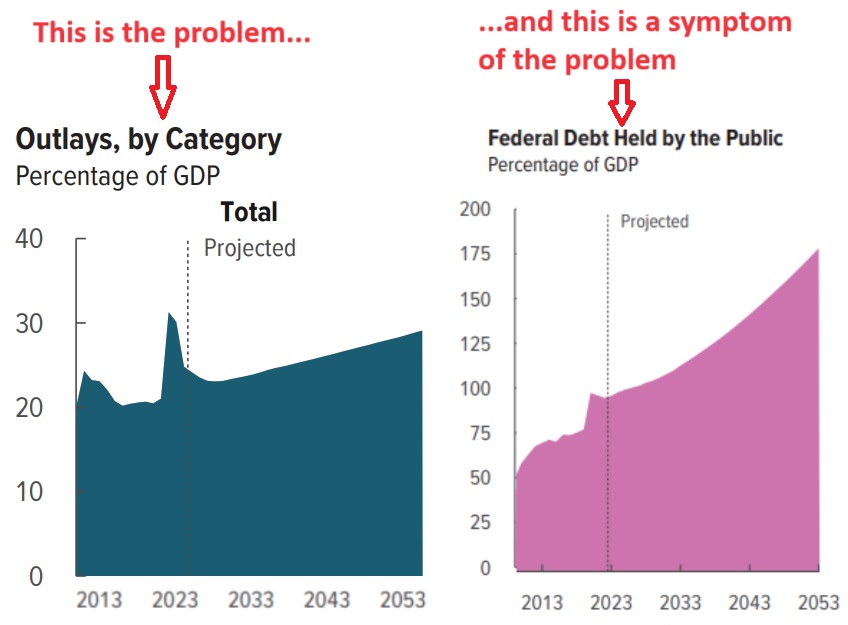

If 51 seconds is too much, here’s a visual I created using the latest long-run forecast from the Congressional Budget Office.

But there are two reasons why I’m revisiting the issue today.

First, Mark Warshawsky of the American Enterprise Institute has a new article explaining that the federal government’s deficit is much bigger if you use accrual accounting rather than cash-flow accounting. Here are some excerpts.

Last week, the Treasury Department released…the massive Financial Report (FR) of the US Government. Using an accrual accounting basis, rather than a cash basis, the FR shows a much poorer picture of the current finances of the federal government than the conventional budget. …The budget deficit under the conventional cash-basis terms increased from $1.4 trillion in 2022 to $1.7 trillion in 2023, or about 6.2 percent of GDP… The alternative measure presented in the FR of…$3.4 trillion in 2023…was double the cash basis deficit.

In other words, the symptom of red ink, measured on an accrual basis, is twice as bad as shown in the official numbers.

But I point this out because the real lesson to be learned is that our spending problem is worse than what is shown in the official numbers (blame entitlements).