Regular readers know that I give Trump mixed grades on economic policy.

He gets good marks on issues such as taxes and regulation, but bad marks in other areas, most notably spending and trade.

Which is why I’ve sometimes asserted that there has been only a small improvement in the economy’s performance under Trump compared to Obama.

But I may have to revisit that viewpoint. The Census Bureau released its annual report yesterday on Income and Poverty in the United States. The numbers for 2019 were spectacularly good, with the White House taking a big victory lap.

Here are the three charts that merit special attention.

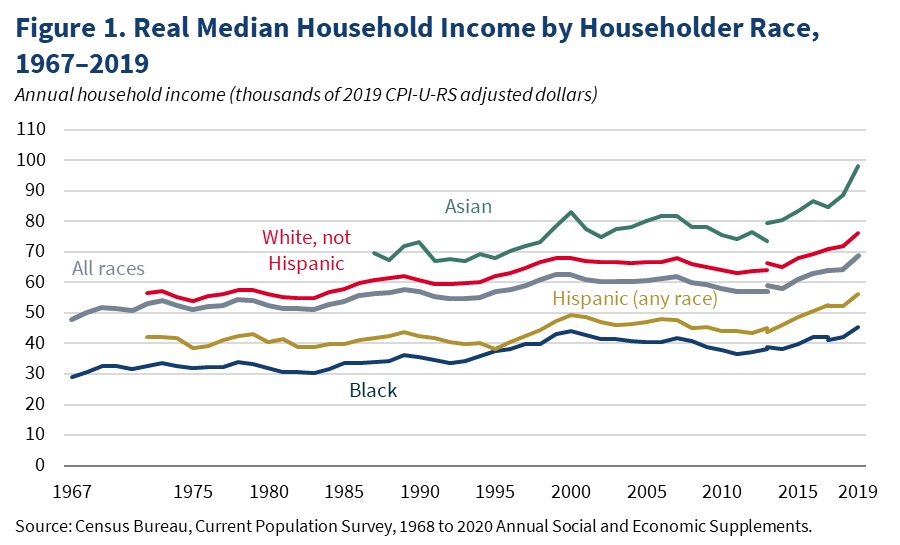

First, we have the numbers on inflation-adjusted median household income. You can see big jumps for all demographic groups.

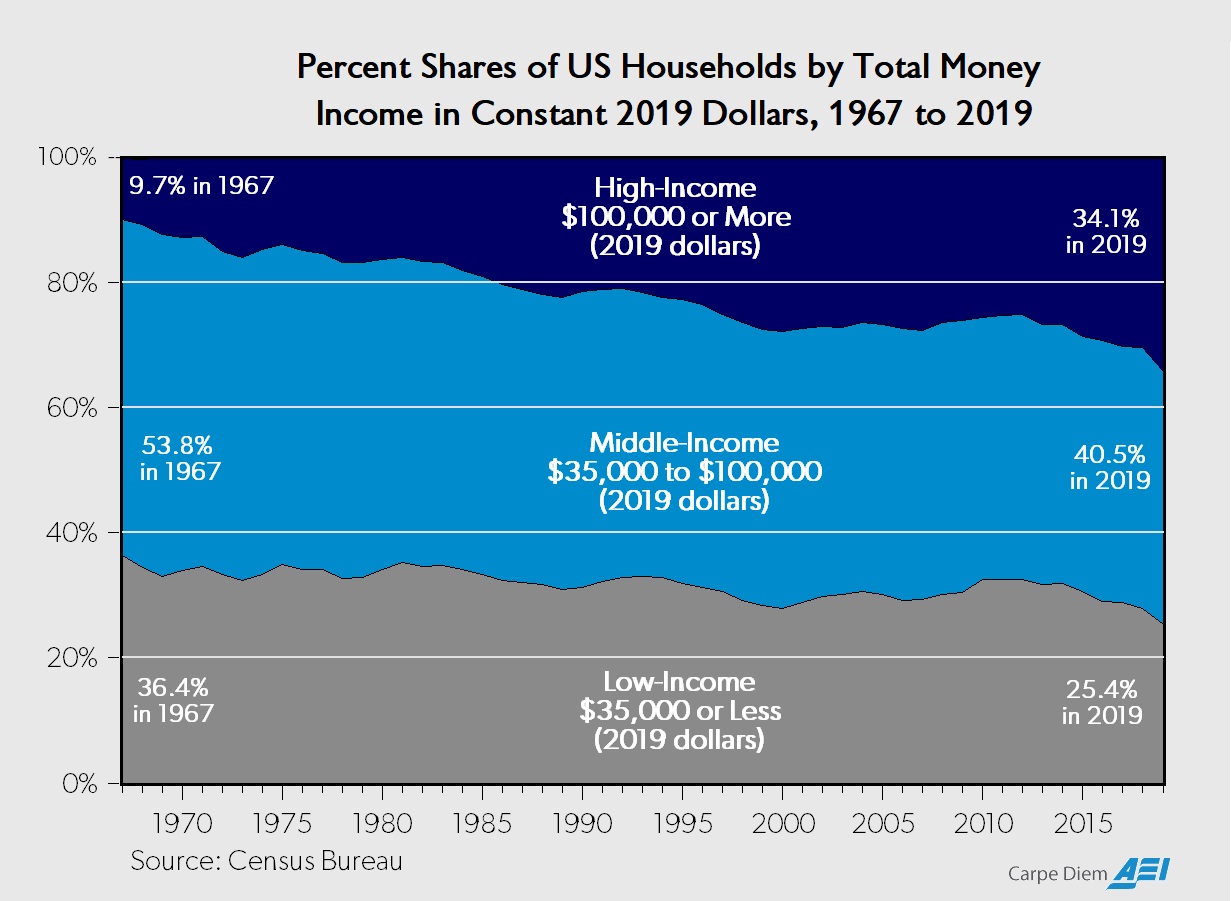

Next, here’s a look at whether Americans are getting richer or poorer over time.

As you can from this chart, an ever-larger share are earning high incomes (a point I made last month, but this new data is even better).

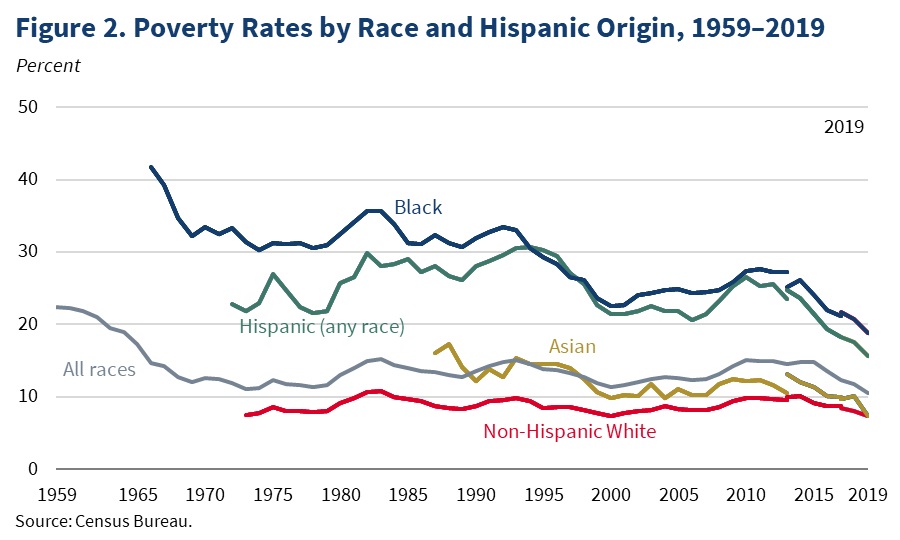

Last but not least, here’s the data on the poverty rate.

Once again, remarkably good numbers, with all demographic groups enjoying big improvements.

We’ll see some bad news, of course, when the 2020 data is released at this point next year. But that’s the result of coronavirus.

So let’s focus on whether Trump deserves credit for 2019, especially since I got several emails yesterday from Trump supporters asking whether I’m willing to reassess my views on his policies.

At the risk of sounding petulant, my answer is no. I don’t care how good the data looks in any particular year. Excessive government spending is never a good idea, and it’s also never a good idea to throw sand in the gears of global trade.

But perhaps we should rethink whether the positive effects of some policies are stronger and more immediate while the negative effects of other policies are weaker and more gradual.

I’ll close with two cautionary notes about “sugar high” economics.

- First, Trump’s fiscal policy of tax cuts and more spending could be viewed as textbook Keynesianism. I definitely don’t think that approach creates more long-run growth, but it can lead to some illusory short-term prosperity as an economy consumes more than it produces.

- Second, I worry that some of last year’s good economic data may have been the result of the Federal Reserve’s easy-money policies. As I’ve previously noted, bubbles always feel good when they’re expanding. They don’t feel so good when they pop.

For what it’s worth, we’re not going to resolve this debate because coronavirus has been a huge, exogenous economic shock.

Though if (or when) the United States ever gets to a tipping point of too much debt, there may be some retroactive regret that Trump (along with Obama and Bush) viewed the federal budget as a party fund.

———

Image credit: The White House | Public Domain.