If Donald Trump wins the 2020 election, I don’t expect any serious effort to rein in the burden of government spending.

And if Joe Biden wins the 2002 election, I don’t expect any serious effort to rein in the burden of government spending.

At the risk of understatement, this is rather unfortunate since fiscal policy in the United States is on a very worrisome path.

At the risk of understatement, this is rather unfortunate since fiscal policy in the United States is on a very worrisome path.

Thanks to demographic changes and poorly designed entitlement programs, the federal budget – assuming it is left on autopilot – is going to consume an ever-larger share of the nation’s economic output.

And that means fewer resources for the economy’s productive sector.

In a new study from the Hoover Institution, Professor John F. Cogan, Daniel L. Heil, and Professor John B. Taylor investigate the potential consequences of bigger government – and the potential benefits of spending restraint.

In this paper we consider an illustrative fiscal consolation proposal that restrains the growth in federal spending. The policy is to hold federal expenditures as a share of GDP at about the 20 percent ratio that prevailed before the pandemic hit.

We estimate the policy’s impact using a structural macroeconomic model with price and wage rigidities and adjustment costs. The spending restraint avoids a potentially large increase in future federal taxes and prevents the outstanding debt relative to GDP from rising from its current level. The simulations show that the consolidation plan boosts short-run annual GDP growth by as much as 10 percent and increases long-run annual GDP growth by about 7 percent.

The authors believe that there will be some tax increases over the next few decades – an assumption that I fear will be accurate.

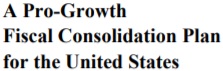

…our baseline assumes that future Congresses will enact tax increases to finance a portion of rising future federal spending. Specifically, we have assumed that Congress will finance half of the projected higher baseline outlays with higher tax rates. The tax rate increases are assumed to be gradually phased-in and are in the form of equi-proportionate increases in personal income tax rates, corporate income tax rates, and social insurance tax rates. Under these assumptions, tax rates will be about 20 percent higher in 2045 than in 2022.

Here are their projection over the next 25 years.

The authors then create an alternative scenario based on spending restraint, including entitlement reform.

To illustrate the potential positive impact of a fiscal consolidation plan on economic growth, we have chosen a stylized long-term budget policy that reduces the growth in federal spending, maintains federal tax rates at their current levels, and limits the outstanding federal debt relative to GDP to its pandemic high level. …the spending side of the plan has three essential elements. One, reductions in government spending from the baseline which come exclusively from permanent changes in entitlement programs; the principal source of the federal government’s long-term fiscal imbalance. …Two, the plan contains an immediate one-time reduction in entitlement program spending that permanently lowers the overall level of government spending. Three, the plan permanently reduces the growth in entitlement spending thereafter from this lower level.

They then estimate what happens to the fiscal burden of government if policy makers choose spending restraint instead of bigger government and tax increases.

In 2033, ten years from the initiation of the policy, total federal spending as a percent of GDP, including interest on the debt, would be 3.3 percent lower than baseline expenditures. In twenty years, it would be 5.7 percent lower. …the consolidation plan would maintain all federal tax rates.at their current statutory levels. …revenue as a share.. of GDP would rise slightly over time due to real bracket creep. Thus, the plan is designed to prevent the approximately 15 percent tax rate increases that are presumed in the budget baseline.

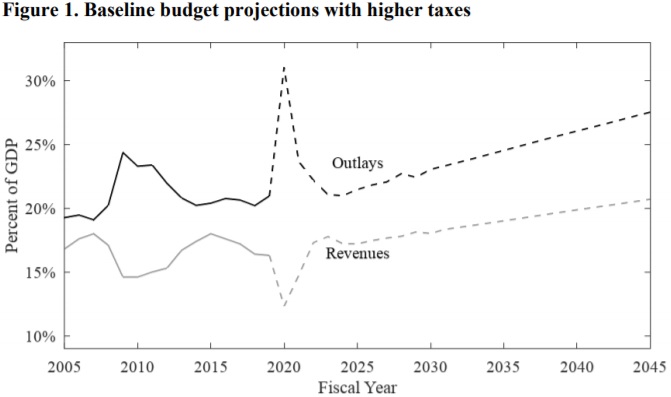

Here’s a chart from the study that shows how the burden of redistribution spending and social insurance programs is significantly smaller with the restraint approach.

Now we get to key results.

Cogan, Heil, and Taylor use a model of the U.S. economy to estimate what happens if there is spending restraint instead of bigger government.

Unsurprisingly, there’s more prosperity when there’s a smaller burden of spending.

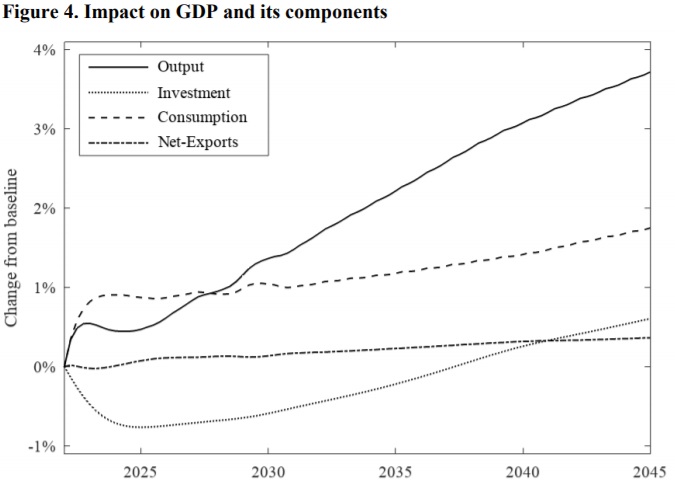

The impact of the consolidation strategy is shown in Figure 4. Observe that there is a substantial increase in real GDP in the short run, and that this positive change occurs throughout the simulation through 2045. The short-run increase of about 0.5 percent in the first two years following the policy’s implementation amounts to about a 10 percent increase in the real GDP growth rate. Over the longer-term, GDP increases by about 3.7 percent after 25 years. This is equivalent to a 7 percent increase in the economy’s real growth rate.

This chart from the study shows the economic benefits of spending restraint.

These results are consistent with what other economists have produced.

Heck, even economists at left-leaning international bureaucracies such as OECD, World Bank, and IMF have acknowledged that smaller government is better for prosperity.

P.S. The unanswered question, of course, is how to convince self-interested politicians to choose spending restraint instead of buying votes with other people’s money. A spending cap is probably a necessary but not sufficient condition (it’s an approach that has been very successful in Switzerland, Hong Kong, and Colorado – and which was recently adopted in Brazil).

P.P.S. Even small differences in economic growth have a significant long-run impact on living standards.

———

Image credit: Bjoertvedt | CC BY-SA 3.