There are many reasons to be depressed about Italy.

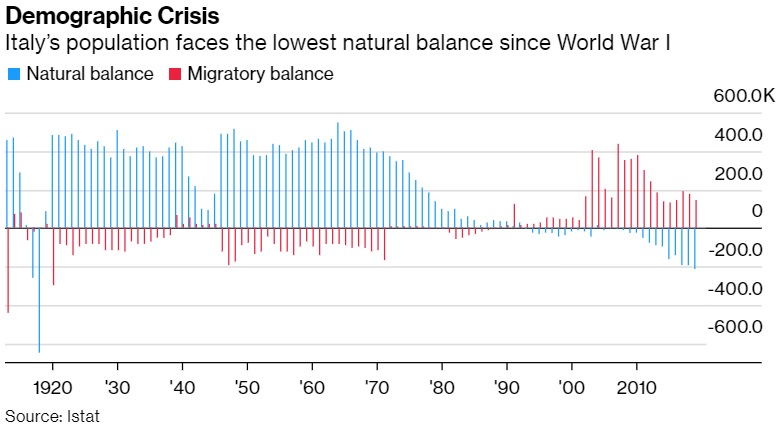

Bad policy is part of the problem, of course, but this chart shows that the country also is facing a demographic crisis. The blue lines show that there are now more deaths than births.

The chart comes from a Bloomberg column by Flavia Rotondi and Giovanni Salzano, and they explain some of the adverse consequences of this demographic change.

Italy isn’t just in an economic slump, its population is also sagging, pushing the country into its biggest demographic crisis in more than a century. The number of people in the country fell for a fifth year in 2019, and deaths exceeded births by almost 212,000, the biggest gap since 1918.

…Italy already has huge long-term economic challenges, and the population trends, if they continue, are going to make surmounting them even harder. Italy won’t have enough young workers, and funding a rapidly aging population will strain an already stretched fiscal situation. Pension costs now amount to almost 17% off the economy. …“With an aging population and a consistent decrease of workers who pay taxes, our retirement system may go haywire” said Pietro Reichlin, a professor of economics.

Politicians naturally will want to compensate for these changes by raising the tax burden.

But Italy already is at a breaking point because of punitive taxation. Writing for the Foundation for Economic Education, Daniel Di Martino discusses his nation’s dirigiste system.

Italy’s problem, similar to many of its southern European neighbors, is an oppressively high tax burden, irresponsible welfare programs that encourage high measured unemployment and increase the debt, and high levels of regulation. …the share of average wages collected by the Italian government via income and social security taxes is 48 percent,

among the highest in the Organization for Economic Co-operation and Development (OECD). In addition, Italy imposes a value-added tax of 22 percent on most goods and services, one of the highest in Europe. Plus, Italy’s corporate, capital gains, gift, and myriad other taxes are passed on to individuals and borne directly by workers. …At the same time, Italy’s complex regulations are a barrier to starting or continuing productive activities. A study by economist Raffaela Giordano of the Bank of Italy concluded that the main reason behind Italy’s underperformance was burdensome regulations and corrupt and inefficient government structure.

Adam O’Neal makes similar points about bad policy in a column for the Wall Street Journal.

Even before the pandemic, Italy hadn’t recovered fully from the 2008-09 financial crisis. Unemployment hovered around 10% in 2019. Adjusting for inflation, the average Italian worker earned the same as he did 20 years ago. Italian banks were Europe’s weakest.

…What ails Italy? …Italy’s greatest challenge is a gargantuan government that destroys wealth as efficiently as the private economy creates it. …In 2018 government revenue was 42% of GDP, nearly 8 points above the Organization for Economic Cooperation and Development average. Yet profligate outlays—Rome spent 16.2% of GDP on public pensions in 2015—brought debt to about 135% of GDP last year.

The net effect of all this misguided policy is that Italy’s economy is moribund.

In his column for Bloomberg, Professor Tyler Cowen summarizes the problem.

One striking fact about Italy is that, over the last 20 years, growth in per capita income has been close to zero. …a zero-growth environment cannot be stable forever. …If the pie doesn’t grow,

eventually it becomes harder to sustain productive activity… Aging is another reason economic growth is necessary. …many countries (including Italy) have expensive pension systems. Someone has to pay the bill, and without innovation and economic growth, taxes will have to rise. That in turn discourages work, pushing people into untaxed black-market activity, necessitating higher tax rates, and the vicious cycle starts again.

And when you combine bad demographics and bad policy, that not only means stagnation in the short run, it also could mean fiscal crisis in the long run.

Except “long run” may be just around the corner.

Desmond Lachman of the American Enterprise Institute warns that an Italian fiscal crisis will make the mess in Greece seem trivial by comparison.

…markets are displaying remarkable complacency toward a rapidly deteriorating Italian political and economic situation. They are doing so in a manner that is painfully reminiscent of how complacent they were in 2009 on the eve of the Greek sovereign debt crisis.

This could have major consequences for global financial markets considering that the Italian economy…has around 10 times as much public debt as Greece had at the time of its crisis. …One has to hope that while markets might be turning a blind eye to Italy’s deteriorating economic and political fundamentals, global economic policymakers are not. As experience with the Greek sovereign debt crisis reaffirmed, crises often take a lot longer than one would have thought to occur, but when they do occur they do so at a very much faster rate than one would have expected.

Some people argue that a fiscal crisis can be avoided if the European Central Bank buys up Italy’s government debt.

That certainly can avert a panic, at least for a while, but this approach can cause a different set of problems.

Joseph Sternberg opines for the Wall Street Journal that the European Central Bank’s easy-money policy has backfired by giving politicians in Rome the leeway to postpone desperately needed reforms.

If the ECB had not stepped in as a buyer of government debt, Rome long since would have faced fiscal catastrophe. Only a miracle—or €365 billion in ECB purchases of Italian sovereign debt since 2015—can explain how in recent years a country whose debt has ballooned to 130% of gross domestic product

paid nearly the same interest rate as Germany… Even after selling so many sovereign bonds to the central bank, Italy’s banks continue to be large holders of their government’s debt. Such bonds constitute around 10% of Italian bank assets, nearly three times the eurozone average. …Mr. Draghi hoped his interventions would give wayward governments such as in Rome breathing room to overhaul the supply side of their economies—deregulating markets, privatizing state assets, trimming welfare programs and the like. But Rome has mainly slid backward.

While intervention by the European Central Bank isn’t the solution to Italy’s problems (and may actually make problems worse), this is also a good opportunity to make the related point that the euro currency also shouldn’t be blamed for the nation’s stagnation.

I’m not a big fan of the European Union and the crowd in Brussels, but Italy’s challenges overwhelmingly are the fault of policies adopted by Italian politicians.

Indeed, if you look at the data from the most-recent edition of the Fraser Institute’s Economic Freedom of the World, you can see monetary policy isn’t a problem. Instead, the nation’s big impediment to prosperity (highlighted in red) is terrible fiscal policy.

To put this data in perspective, Italy has the next-to-lowest-ranked economy in Western Europe, with only Greece having less economic liberty.

The numbers from the Heritage Foundation’s Index of Economic Freedom tell a very similar story.

If you peruse the data from the most-recent edition of that publication, you’ll see that Italy gets weak scores for its approach to labor issues, the judiciary, and taxes.

But it gets an utterly dismal score (highlighted in red) for government spending.

Sadly, there’s no political party in Italy that wants to solve the problem of excessive spending – even though I explained how it could be done while in Milan many years ago. And without spending restraint, that means it’s almost impossible to adopt pro-growth tax reform.

P.S. No wonder some people in Sardinia want to secede from Italy and instead become part of Switzerland.

P.P.S. Amazingly, a New York Times’ columnist actually argued that the United States should be more like Italy.

———

Image credit: Pedro Ribeiro Simões | CC BY 2.0.