Having been exposed to scholars from the Austrian school as a graduate student, I have a knee-jerk suspicion that it’s not a good idea to rely on the Federal Reserve for macroeconomic tinkering.

In this interview from yesterday, I specifically warn that easy money can lead to economically harmful asset bubbles.

Since I don’t pretend to be an expert on monetary policy, I’ll do an appeal to authority.

Claudio Borio of the Bank for International Settlements is considered to be one of the world’s experts on the issue.

Here are some excerpts from a study he recently wrote along with three other economists. I especially like what they wrote about the risks of looking solely at the price level as a guide to policy.

The pre-crisis experience has shown that, in contrast to common belief, disruptive financial imbalances could build up even alongside low and stable, or even falling, inflation. Granted, anyone who had looked at the historical record would not have been surprised: just think of the banking crises in Japan, the Asian economies and, going further back in time, the US experience in the run-up to the Great Depression. But somehow the lessons had got lost in translation… And post-crisis, the performance of inflation has repeatedly surprised. Inflation…has been puzzlingly low especially more recently, as a number of economies have been reaching or even exceeding previous estimates of full employment. …the recent experience has hammered the point home, raising nagging doubts about a key pillar of monetary policymaking. …Our conclusion is that…amending mandates to explicitly include financial stability concerns may be appropriate in some circumstances.

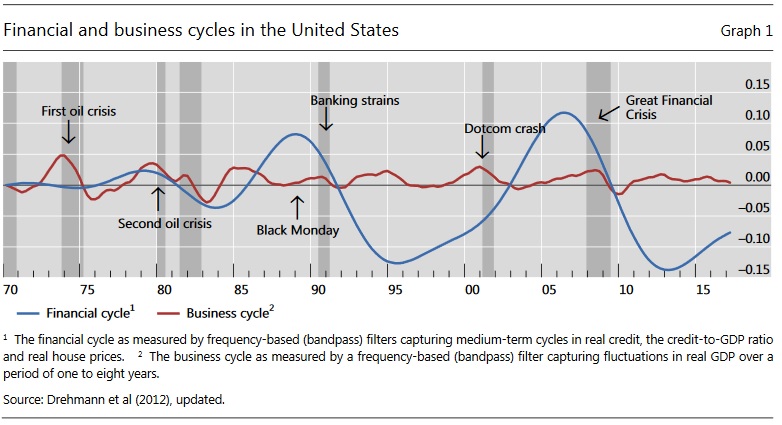

Here’s a chart showing that financial cycles and business cycles are not the same thing.

The economists also point out that false booms instigated by easy money can do a lot of damage.

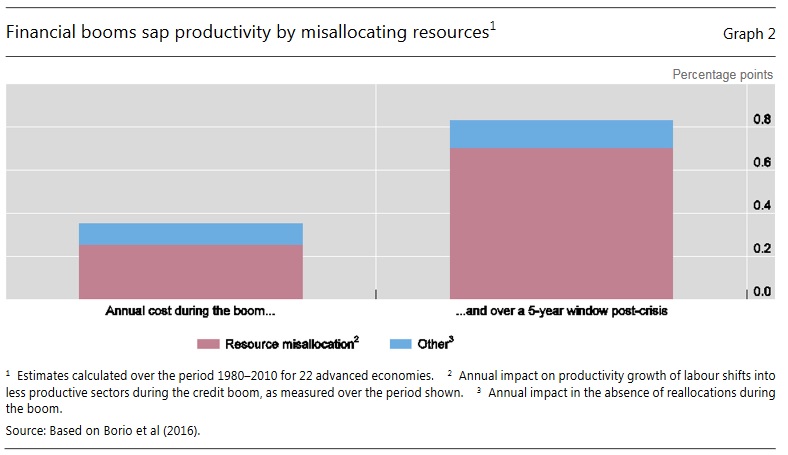

Some recent work with colleagues sheds further light on some of the possible mechanisms at work (Borio et al (2016)). Drawing on a sample of over 40 countries spanning over 40 years, we find that credit booms misallocate resources towards lower-productivity growth sectors, notably construction, and that the impact of the misallocations that occur during the boom is twice as large in the wake of a subsequent banking crisis. The reasons are unclear, but may reflect, at least in part, the fact that overindebtedness and a broken banking system make it harder to reallocate resources away from bloated sectors during the bust. This amounts to a neglected form of hysteresis. The impact can be sizeable, equivalent cumulatively to several percentage points of GDP over a number of years.

Here’s a chart quantifying the damage.

And here’s some more evidence.

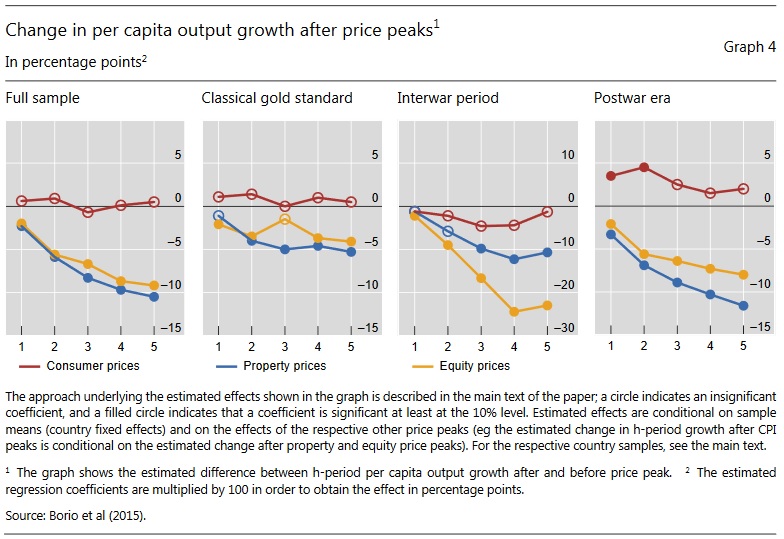

In recent work with colleagues, we examined deflations using a newly constructed data set that spans more than 140 years (1870–2013), and covers up to 38 economies and includes equity and house prices as well as debt (Borio et al (2015)). We come up with three findings. First, before controlling for the behaviour of asset prices, we find only a weak association between deflation and growth; the Great Depression is the main exception. Second, we find a stronger link with asset price declines, and controlling for them further weakens the link between deflations and growth. In fact, the link disappears even in the Great Depression (Graph 4). Finally, we find no evidence of a damaging interplay between deflation and debt (Fisher’s “debt deflation”; Fisher (1932)). By contrast, we do find evidence of a damaging interplay between private sector debt and property (house) prices, especially in the postwar period. These results are consistent with the prevalence of supply-induced deflations.

I’ll share one final chart from the study because it certainly suggest that the economy suffered less instability when the classical gold standard was in effect before World War I.

I’m not sure we could trust governments to operate such a system today, but it’s worth contemplating.

P.S. I didn’t like easy money when Obama was in the White House and I don’t like it with Trump in the White House. Indeed, I worry the good economic news we’re seeing now could be partly illusory.