In pure socialist systems, governments own and operate companies (the “means of production“). Such an approach also requires central planning and price controls.

But you don’t need socialism to have government-controlled companies. There are plenty of “state-owned enterprises” that exist in supposedly market-oriented nations.

Including in the United States. The federal government, for instance, owns and operates the air traffic control system and the postal service, to cite two big examples.

So what happens when politicians are de facto shareholders?

Today, thanks to some new research from the Asian Development Bank Institute, we’re going to look at the economic consequences of such firms.

Throughout history, and especially since the end of World War II, state-owned enterprises (SOEs) have been created in much of the world… Although private companies play a dominant role in market-based societies, enterprises with government ownership

are still key players in the global economy, making their performance important for economic growth and competitiveness… Thus, scholars and policymakers around the world have been left with a task of reassessing the efficiency of state ownership. …In this paper, we aim to investigate whether certain ownership types consistently show superior economic performance relative to others when controlling for other economic factors. …we aim to fill in this gap and report further empirical evidence on the relative efficiency of public and private companies.

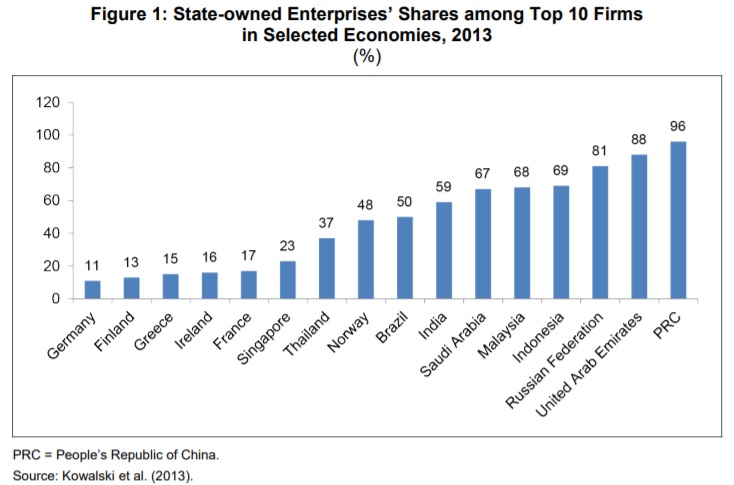

According to the study, state-run companies play a very large role in some countries.

The authors consider some of the theoretical reasons why state-run firms might not be very efficient, including “public choice.”

Agency theory…states that in a corporation, managers (or agents) may follow a personal agenda rather than work on behalf of, and for the interest of, the principals who own the corporation. Within a SOE, in particular, …the managers of SOEs are those who are appointed by the government…and seek firm-specific rents, such as high pay, fringe benefits, and low effort levels. Unlike their peers who operate in private-owned enterprises and may face the risk of replacement and dismissal due to their firms’ low performance…, the chief executive officers (CEOs) of SOEs are put under little financial constraint, and their compensation is not necessarily linked to firm performance… Public choice theory…also provides a cornerstone conceptual framework on which SOEs’ underperformance can be explained. This framework assumes that…special interests affect…governments’ own objectives.

They put together a dataset of more than 25,000 companies, both government and private, and then looked at key performance metrics.

Not surprisingly, government-run firms are not very efficient compared to their private counterparts.

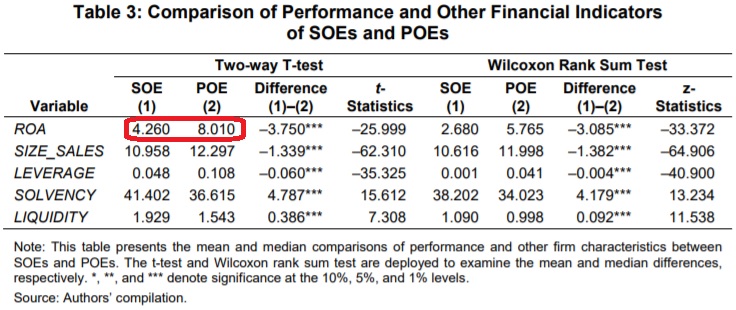

…we find significant evidence that SOEs are outperformed by their POEs counterparts. The findings are consistent over both simple univariate comparisons and multivariate regressions. Government firms appear to be less profitable than POEs. They are also more dependent on debt and financial support from outside sources rather than equity. Hence, we provide support for the view that public firms are less efficient than private firms… The cross-sectional comparisons also show that government firms tend to be more labor intensive and have higher labor costs than non-government ones. …The differences in profitability appear to be economically important. The average return on assets for private firms is 8.010, almost twice that for SOEs. …SOEs have a higher liabilities-to-assets ratio, meaning that they tend to rely more on debt than shareholder funds. … state-owned companies…generate smaller sales volumes and have a higher cost per one employee. In other words, firms owned by private sectors are more labor efficient than government ones. …our findings suggest that privatization could be considered as a driver for firm efficiency.

For those that like perusing quantitative results, here are the results of their statistical regressions.

I’ve highlighted the key difference.

As already noted, government-run firms accumulate more debt.

This is presumably because investors assume that government-run companies won’t default.

Not because they don’t lose money, but rather because the political pressures that led to their creation also will prevent their demise.

SOEs can enjoy a “soft” budget constraint since they are backed by the government for their funding… They have the advantage of borrowing funds at a lower rate rather than accessing the equity market to raise capital… Thus, the discipline that capital markets impose on state-held firms and the threat of financial distress for them is less important than their private counterparts. …it is worth noting that such “soft” budget constraints, to a certain extent, could also be a source of inefficiency in government firms.

In other words, the growth-enhancing process of “creative destruction” is blocked when governments are in charge of companies.

For what it’s worth, this is a big problem in nations such as China.

Though we also saw a version of this in the United States, with the big bailouts of Fannie Mae and Freddie Mac, both of which are government-sponsored enterprises (private ownership, but created by government and controlled by government).

And there are many other examples of bad results when the federal government has intervened in the business world.

The bottom line is that government should not be owning, operating, controlling, or directing private companies. These forms of intervention inevitably produce inefficiency, subsidies, cronyism, corruption, and waste.

And it means that people like you and me wind up with less income and lower living standards because politicians are misallocating labor and capital.