The Trump tax plan, which was signed into law right before Christmas in 2017, had two very good features.

- Restricting the deduction for state and local taxes.

- A reduction of the corporate tax rate to 21 percent.

The former was important because the federal tax code was subsidizing high tax burdens in states such as New Jersey, Illinois, and California.

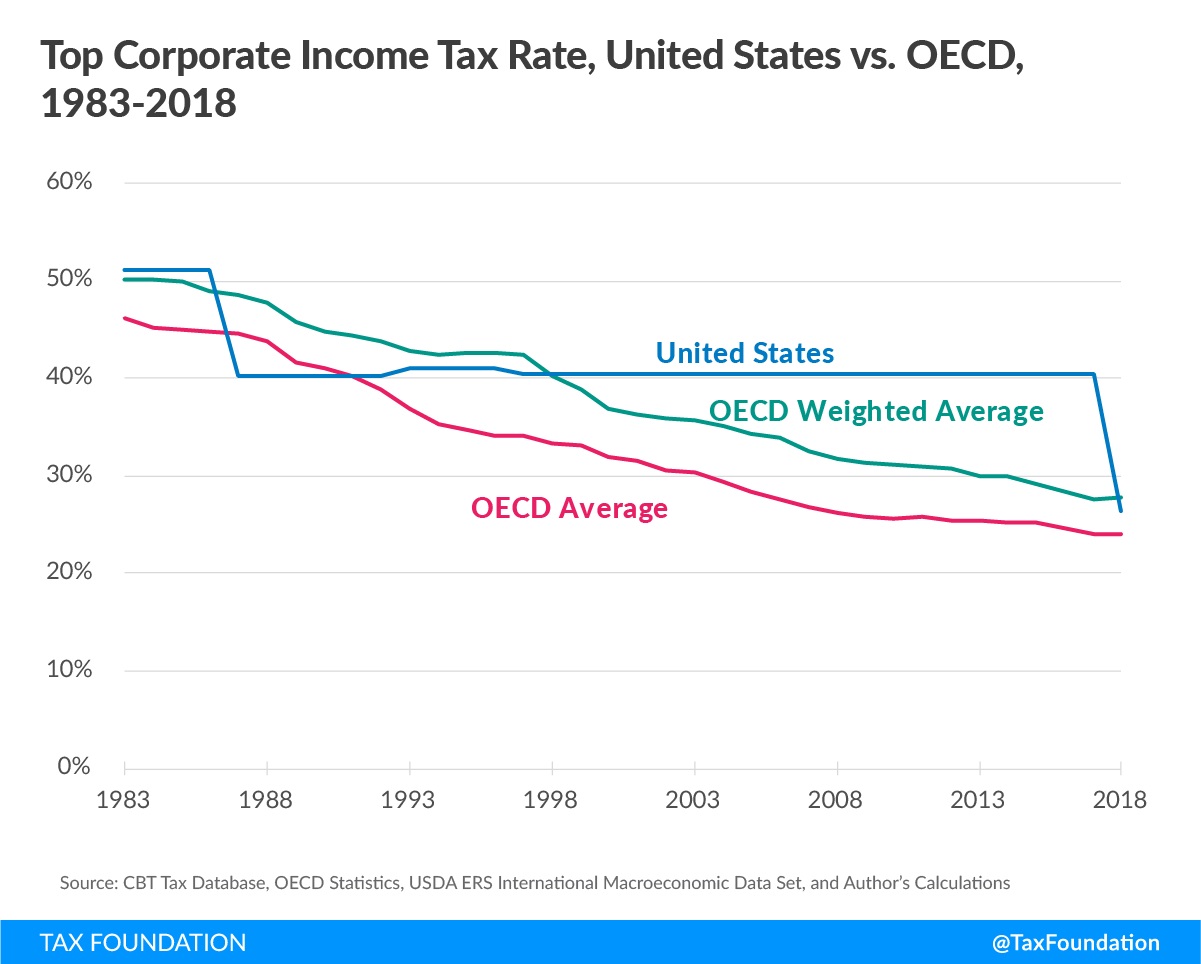

The latter was important because the United States, with a 35 percent corporate rate, had the highest tax burden on businesses among developed nations.

The 21 percent rate we have today doesn’t make us a low-tax nation, but at least the U.S. corporate tax burden is now near the world average.

There were many other provisions in the Trump tax plan, most of which moved tax policy in the right direction.

Now that a couple of years have passed, what’s been the net effect?

In a column for today’s Wall Street Journal, former Trump officials Gary Cohn and Kevin Hassett make the case that the tax plan has produced good results.

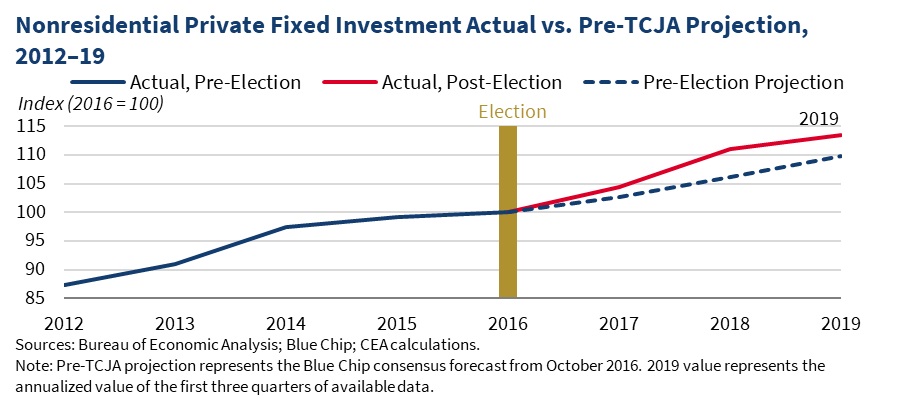

…the tax cut reduced the cost of installing new plant and machinery by about 10%, suggesting that capital spending would jump by the same amount. This would increase the amount of capital per worker and drive up productivity and wages. …This predicted increase in capital has materialized, and has translated into additional economic growth. …Capital spending was 4.5% higher in 2018 than pre-TCJA blue-chip forecasts, and this trend continued in 2019.

This extra capital improved productivity and wages… Over the past year, nominal wages for the lowest 10% of American workers jumped 7%. The growth rate for those without a high-school diploma was 9%. …when President Obama hiked marginal tax rates, …labor-force participation dropping 0.7% after the tax increase for workers 35 to 44, but dropping 1.5% for workers over 55. After passage of the TCJA, the opposite pattern emerged, with labor-force participation for those between 35 and 44 increasing 0.4%, and labor-force participation for those over 55 increasing 1.3%. … Before Mr. Trump took office in January 2017, the Congressional Budget Office forecast the creation of only two million jobs by this point. The economy has in fact created seven million jobs since January 2017. …the U.S. is the only Group of Seven country that will post growth above 2% this year.

And the White House has been publicizing some positive numbers.

Such as an increase in investment.

I suppose one can argue that the Blue Chip consensus forecast was wrong and that the Trump tax plan had no effect, but that seems like an after-the-fact rationalization.

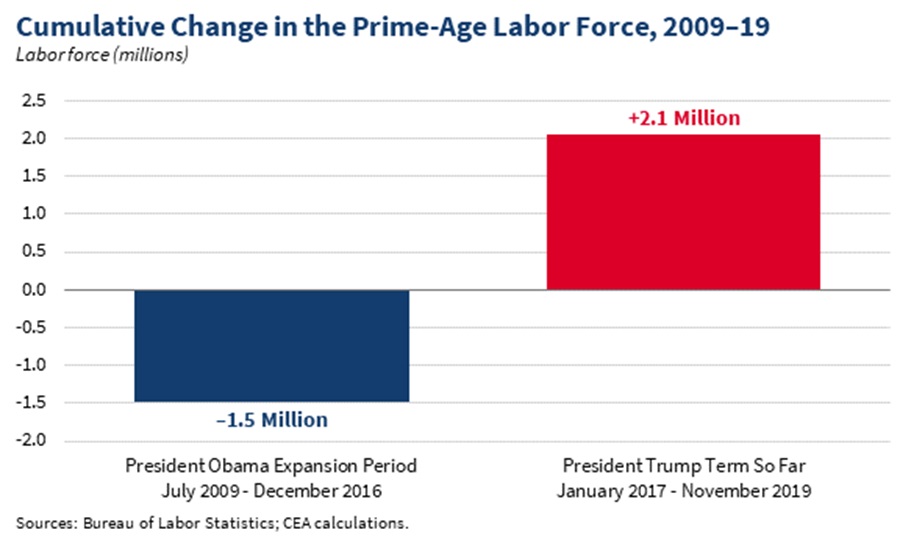

The White House also has been touting an increase in prime-age labor force participation.

These are impressive numbers. I’ve argued, for instance, that the employment/population ratio may now be a more important variable than the unemployment rate.

Regardless, the best numbers I’ve seen aren’t from the White House.

Andy Puzder recently shared this chart showing that workers in low-wage industries (the blue line) are enjoying the biggest gains.

I want everyone’s wages to increase, which is why I’m a big supporter of reforms that boost investment and productivity.

But I especially applaud when those reforms increase wages for those with modest incomes.

I’ll close with three caveats.

- Because Trump has been very weak on the issue of government spending, it’s quite likely that his tax cuts eventually will be repealed or offset by other tax increases.

- Trump obviously was talking nonsense when he claimed his tax plan would produce annual growth of 4 percent or higher. That being said, even more-modest increases in growth are very desirable.

- Trump’s tax increases on trade are bad for prosperity and therefore are offsetting some of the benefits of his tax reductions on corporate and household income.

The bottom line is that Trump has made tax policy better (or less worse), but always remember that tax policy is just one piece of a large puzzle when looking at economic policy.

———

Image credit: The White House | Public Domain.