There are some charming traditions, like the swallows returning every year to the Mission of San Juan Capistrano.

But other traditions are far less impressive, most notably the make-believe hysteria that occurs every time the federal government approaches its “debt limit.”

High-level government officials will publicly fret that a failure to increase the limit will produce an unprecedented calamity because the Treasury Department will be forced to default on U.S. government debt, thus triggering a global panic.

And this triggers anxiety in predictable quarters.

A story in USA Today is representative of the sky-is-falling mentality.

Congress will confront a potentially devastating financial crisis in September as lawmakers scramble to…prevent the nation from defaulting on its debt for the first time in history. …The debt limit, set by Congress, is the legal amount the U.S. Treasury can borrow to pay the government’s existing bills, including Social Security and Medicare benefits, military salaries, tax refunds, interest on the national debt, and other obligations. The government has never defaulted on its debt before, and no one knows for sure what the impact would be. However, economists warn that it could plunge the U.S. back into recession and spark a global economic crisis.

Paul Krugman is predictably hysterical about the prospect.

The odds of a self-inflicted US debt crisis now look pretty good: hard-line Republicans are eager to hold the economy hostage… So it looks fairly likely that by October or so there will come a day when the U.S. government stops paying some of its bills, including interest on debt. How bad will that be? The truth is that we don’t know.. Until now, US debt has played a special role in the world economy, because it is — or was — the ultimate safe asset, the thing people can use to secure transactions with no questions about it retaining its value. …Taking away that role could be very nasty.

Even some establishment voices are fanning the flames, including Maya MacGuineas of the Committee for a Responsible Federal Budget.

Our economic standing is too sterling and the global economy too important to imperil over the disagreements of American domestic politics — as fundamental as they may be. It is the height of recklessness — a view held for decades reflected in the fact that raising the debt ceiling was once a mundane piece of housekeeping that garnered no attention. It was practically automatic.

And Professor Edward Kleinbard of the University of Southern California also thinks the apocalypse is nigh.

Sometime in October, the United States is likely to default on its obligation to pay its bills as they come due, having failed to raise the federal debt ceiling. This will cost the Treasury tens of billions of dollars every year for decades to come in higher interest charges and probably trigger a severe recession. …almost all economists and policy makers agree on the enormous fiscal, economic and reputational costs of default. That’s why, in the past, we’ve always managed to avoid it.

Sounds ominous, right?

And I agree that it would be very bad news if the U.S. government didn’t pay all interest and principal to bondholders, as scheduled.

But here’s the good news. The odds of that happening are about the same as the odds of me being the keynote speaker at the next convention of the Socialist Party.

As I’ve said over the years in television interviews, at press conferences, and in congressional testimony (on more than one occasion), there won’t be a default for the simple reason that the federal government collects far more money than needed to pay all bondholders without any delay.

And nothing has happened to the budget numbers to change that analysis.

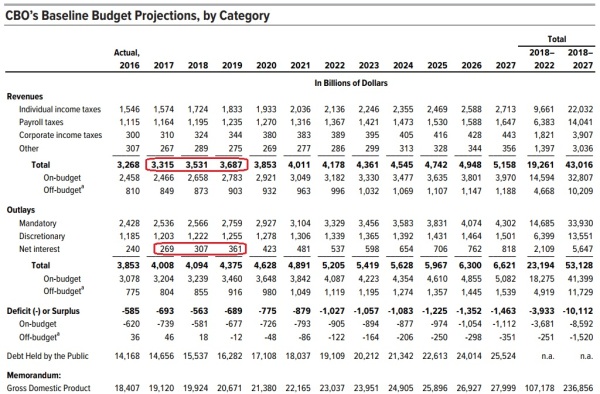

Here are the latest CBO projections on major budget aggregates. I’ve circled total tax receipts for the next three years, as well as annual net interest payments. As you can see, the Treasury will be collecting more than 10 times as much revenue as needed to fulfill obligations to the folks who have lent money to Uncle Sam.

By the way, some of you may be thinking I’m a cranky libertarian who is blind to the danger of default.

Well, I am a libertarian, and I do get cranky about the various shenanigans in Washington, so let me engage in what’s known as an “appeal to authority.”

Here’s what the Congressional Budget Office said in its recent report on the debt limit.

When Would the Extraordinary Measures and Cash Run Out, and What Would Happen Then? If the debt limit is not increased above the amount that was established on March 16, 2017, the Treasury will not be authorized to issue additional debt that increases the amount outstanding. …That restriction would ultimately lead to delays of payments for government programs and activities, a default on the government’s debt obligations, or both.

In other words, the government can choose to pay interest on the debt and defer other bills. As I’ve repeatedly said in all my public pronouncements, a default will occur only if an administration wants it to occur.

But that’s not going to happen. Just as Obama’s various Treasury Secretaries would have “prioritized” payments to bondholders, Trump’s Treasury Secretary will do the same thing if push comes to shove.

Some budget experts on the left know this is true so they try to blur the issue by stating that it is “default” to postpone payment on any type of government spending. Here’s some of what Kleinbard wrote in his column.

…some conservative policy makers besides Mr. Mulvaney have convinced themselves that crashing into the debt ceiling won’t be a big deal because the government can “prioritize” its bill payments, so that interest on Treasury debt will be paid on a current basis, while other bills sit unpaid. Understanding the false allure of prioritization requires a little background. …there are profound doubts as to whether the Treasury could even implement prioritization, beyond ring fencing interest payments, because its payment systems are designed to pay all claims as they are due, regardless of their origin. More important, prioritization is default by another name. The consequences are the same, regardless of which i.o.u.s Treasury chooses to dishonor. All valid claims against the United States are backed by the credit of the United States… The deliberate nonpayment of billions of dollars of uncontested claims every month thus constitutes default, even if the Treasury is paying some of its other debts.

The last sentence in the above excerpt is bunk. Postponing or deferring bills is not good budget policy. It’s basically what happens in poorly governed places like Greece and Illinois. But it’s not default. There wouldn’t be any risk to financial markets if the Treasury Department was late in disbursing farm subsidy checks or Medicaid reimbursements.

Let’s close by indulging one of my fantasies. If Donald Trump wanted to force good policy from Congress, he could threaten to veto any debt limit that wasn’t accompanied by something desirable such as a spending cap or entitlement reform. The politicians on Capitol Hill would balk of course, but Trump could shrug his shoulders and start “prioritization” once the debt limit was reached. So long as all bondholders received promised payments, there would be no danger to financial markets. By contrast, however, the various interest groups feeding at the federal trough would begin to squeal once their checks started slowing down. At some point, Congress would be forced to capitulate.

In other words, Trump has the capacity to score a big victory on the debt limit, just like he has the unilateral ability to score a big victory on Obamacare repeal and/or the 2018 spending bills.

I’m not holding my breath for this to happen, but it’s nice to dream. Especially since a big fight over the debt limit today (if successful) could save us from something far worse in the future.

———

Image credit: Andy Withers | CC BY-NC-ND 2.0.